When the first production licences were awarded in the mid-1960s, hardly anyone realised what the industry would mean for the Norwegian economy. Fifty years later, it is more important than ever.

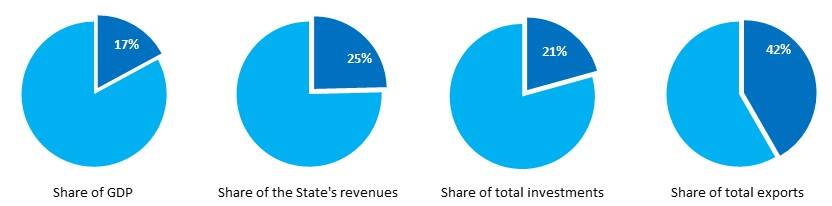

The industry plays a vital role in the Norwegian economy and the financing of the Norwegian welfare state. The oil and gas sector is Norway's largest measured in terms of value added, government revenues, investments and export value. Long-term perspective in the management of the government's petroleum revenues ensures that they benefit Norwegian society as a whole, and that future generations will benefit from Norway’s petroleum wealth. This has been a key principle in developing the financial and legal framework for the sector.

Since production started on the Norwegian continental shelf in the early 1970s, petroleum activities have contributed to over NOK 26 000 billion in current NOK to Norway’s GDP. This does not include related service and supply industries. Yet so far, only about half of the estimated recoverable resources on the Norwegian shelf have been produced and sold.

Macroeconomic indicators for the petroleum sector, 2026

Updated: 15.10.2025

The service and supply industry is not included (Source: Ministry of Finance )

One of the overall principles of Norway’s management of its petroleum resources is that exploration, development and production must result in maximum value creation for society, and that revenues must accrue to the Norwegian state and thus benefit society as a whole. The main reason for this is the extraordinary returns that can be obtained by producing petroleum resources. Since these resources belong to society as a whole, the Norwegian state secures a large share of the value creation through taxation and the system known as the State’s Direct Financial Interest (SDFI) in the petroleum industry.

The expected net government cash flow from petroleum activities (billion NOK, nominal values)

| 2025 | 2026 | |

| Taxes | 373,1 | 291,5 |

| Environmental taxes and area fees | 9,2 | 11,0 |

| Net cash flow from SDFI | 238,9 | 193,0 |

| Equinor dividend | 34,6 | 25,8 |

| Net government cashflow | 655,8 | 521,3 |

(Source: Ministry of Finance, Prop. 26 S (2025-2026) and National Budget 2026)

The total payment form tax revenues and fees from petroleum activities are estimated to NOK 303 billion in 2026. The net cash flow from direct ownership in fields through the SFDI system is estimated to around NOK 193 billion. The government has additional income from Equinor dividend at around NOK 26 billion in 2025. Estimated total net cash flow from the petroleum industry in 2025 is NOK 521 billion.

The net government cash flow from petroleum activities, 1971-2024

Updated: 15.10.2025

Realised net government cash flow. Paid taxes are adjusted for repayments, and the numbers are in constant 2026-prices.

Source: Ministry of Finance, Statistics Norway

Print illustration Download data The net government cash flow from petroleum activities, 1971-2024 Download PDF Download as image (PNG)

High Contrast Mode

Government revenues from petroleum activities are transferred to the Government Pension Fund Global, which at the end of 2025 had holdings with a total value of around NOK 21 300 billion. Under the fiscal rule, transfers can be made to the fiscal budget from the Fund to finance important public goods without drawing on the Fund’s capital.

Macroeconomic indicators for the petroleum sector, 1971-2026

Updated: 15.10.2025

2025 og 2026 are preliminary numbers from the National Budget 2026

Source: Statistics Norway (National accounts), Ministry of Finance (National Budget 2026)

Print illustration Download data Macroeconomic indicators for the petroleum sector, 1971-2026 Download PDF Download as image (PNG)

High Contrast Mode

The petroleum taxation system is based on the rules for ordinary company taxation and are set out in the Petroleum Taxation Act (Act of 13 June 1975 No. 35 relating to the taxation of subsea petroleum deposits, etc). Because of the extraordinary returns on production of petroleum resources, the oil companies are subject to an additional special tax. The current ordinary company tax rate is 22 %. To ensure a neutral taxation system, paid company tax is written off when calculating the special tax base. This entails a special tax rate of 71,8 % in order to maintain a combined marginal tax rate of 78 %. In 2026, Norway’s tax revenues from petroleum activities is estimated to NOK 291,5 billion.

See article about the petroleum tax system for more information.

The State’s Direct Financial Interest (SDFI) is a system under which the Norwegian state owns holdings in a number of oil and gas fields, pipelines and onshore facilities. For oil and gas fields, the proportion is determined when production licences are awarded, and varies from field to field. As one of several owners, the government covers its share of investments and costs, and receives a corresponding share of the income from production licences.

The SDFI system was established on 1 January 1985. Before this, the Norwegian government only had ownership interests in production licences through Equinor (Statoil). From 1985, these were split in two: one part became the State’s Direct Financial Interest (SDFI) and the other part remained with Equinor.

When Equinor was listed on the stock exchange in 2001, the responsibility for managing the SDFI portfolio was transferred from Equinor to a new state-owned management company, Petoro. At the end of 2025 the SDFI portfolio consisted of financial interests in 187 production licences, 48 producing fields and holdings in 16 joint ventures that own pipelines and onshore facilities.

Net cash flow from SDFI in 2026 is estimated to around NOK 193 billion.

")

The Norwegian state owns 67 % of the shares in Equinor, and receives dividends in the same way as other shareholders. In 2026, expected dividend paid to the state is around NOK 25,8 billion.

Area fees

The area fee is intended to ensure that awarded acreage is explored efficiently. In 2026, a total of NOK 1.6 billion is expected paid in area fees.

Environmental taxes

The carbon tax and the NOx tax are important environmental taxes in the petroleum sector. The petroleum industry is also included in the emissions trading system. Companies that are licensees on the Norwegian shelf must therefore purchase emission allowances if their greenhouse gas emissions exceed their allocated amount for the year.

Norway was one of the first countries in the world to introduce a carbon tax, in 1991. This is levied on all combustion of gas, oil and diesel in petroleum operations on the continental shelf and on releases of CO2 and natural gas, in accordance with the CO2 Tax Act on Petroleum Activities. For 2025, the tax rate is estimated to NOK 2.21 per standard cubic metre of gas and NOK 2,51 per litre of oil or condensate. For combustion of natural gas, this is equivalent to NOK 944 per tonne of CO2. For emissions of natural gas, the tax rate is NOK 20,17 per standard cubic metre.

The expected total tax levied is NOK 9,4 billion in 2026.

See article about emissions to air from petroleum activities for more information.